The United States dollar has experienced significant declines in recent months, raising questions about its future trajectory and what this means for global economies. While currency fluctuations are a normal part of financial markets, the current drop in the dollar is particularly dramatic, prompting analysis from economists and market strategists.

The primary drivers behind the dollar’s weakening stem from a complex interplay of factors, beginning with the policies of the Trump administration. Following his election in 2016, the dollar initially strengthened due to expectations of increased US economic growth spurred by potential tax cuts and looser regulations. However, as President Trump pursued trade tariffs against countries like China, significant uncertainty arose regarding the impact on global trade and US economic expansion. These tariffs were designed to boost domestic manufacturing but instead triggered retaliatory measures from other nations, leading to a slowdown in overall economic growth.

Specifically, the ‘Liberation Day’ tariffs announced in August 2018, targeting Chinese steel and aluminum imports, created considerable market turbulence. The initial reaction was a sharp sell-off in US stocks and government bonds, alongside a substantial drop in the dollar’s value. This decline reflects investor concern that these tariffs would negatively impact economic growth, forcing the Federal Reserve to reconsider its monetary policy stance – potentially pausing interest rate hikes or even cutting rates.

The prospect of lower interest rates makes the dollar less attractive to investors seeking higher returns on their capital. Traditionally, a rising dollar is seen as a safe haven investment, but the combination of trade uncertainty and concerns over economic growth has shifted this dynamic. Furthermore, President Trump’s repeated criticisms of Federal Reserve Chair Jerome Powell for not cutting interest rates have added pressure to the greenback.

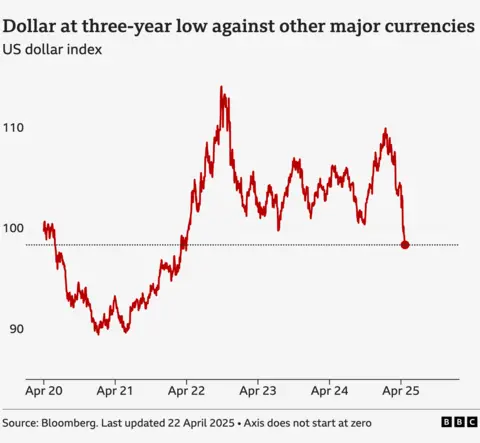

The dollar index, which measures its strength against a basket of major currencies, has fallen to its lowest level in three years, signaling a significant shift in market sentiment. This decline highlights the dollar’s vulnerability and raises questions about its role as the world’s primary reserve currency. The US dollar’s dominance in international trade – approximately half of all global trade invoices are denominated in dollars – amplifies the impact of any weakening trend.

The implications of a weaker dollar are far-reaching. For ordinary Americans traveling abroad, it means their money will buy less, increasing the cost of foreign travel and purchases. Conversely, foreign tourists visiting the US will find their currency goes further. Internationally, a weaker dollar makes US exports cheaper for other countries but can lead to higher import costs in the United States. Many commodities, including oil and gas priced in dollars, benefit from a weaker dollar as they become more affordable for nations using alternative currencies.

The current situation is unusual because the dollar has historically been viewed as a safe haven asset during times of economic uncertainty. However, recent market movements—including the sell-off in US government bonds alongside the dollar’s decline—suggest a broader reassessment of the US economy and its global standing. The ongoing conflict between Trump and Fed Chair Powell further complicates matters, raising concerns about the central bank’s independence from political pressure. While some analysts believe the dollar will regain ground over the coming weeks, it is unlikely to return to previous levels without a resolution to the trade tensions and improved economic outlook. The markets will continue to closely monitor President Trump’s actions towards the Federal Reserve as any potential changes could significantly impact the dollar’s trajectory.